The federal program known as Old‑Age, Survivors, and Disability Insurance (OASDI) — the core of what many recognize as Social Security in the U.S. — is undergoing important updates. From trust-fund projections, payroll tax thresholds, benefit adjustments to regulatory and legislative changes, staying up to date on “social security OASDI updates” is more important than ever for workers, retirees, disabled individuals and survivors alike.

In this article you’ll find:

- The most significant recent updates to OASDI

- Why these updates matter for you now and going forward

- Expert legal counsel resources for benefit, planning or appeal questions

- Practical steps you should take in light of these changes

Key OASDI Updates You Should Know

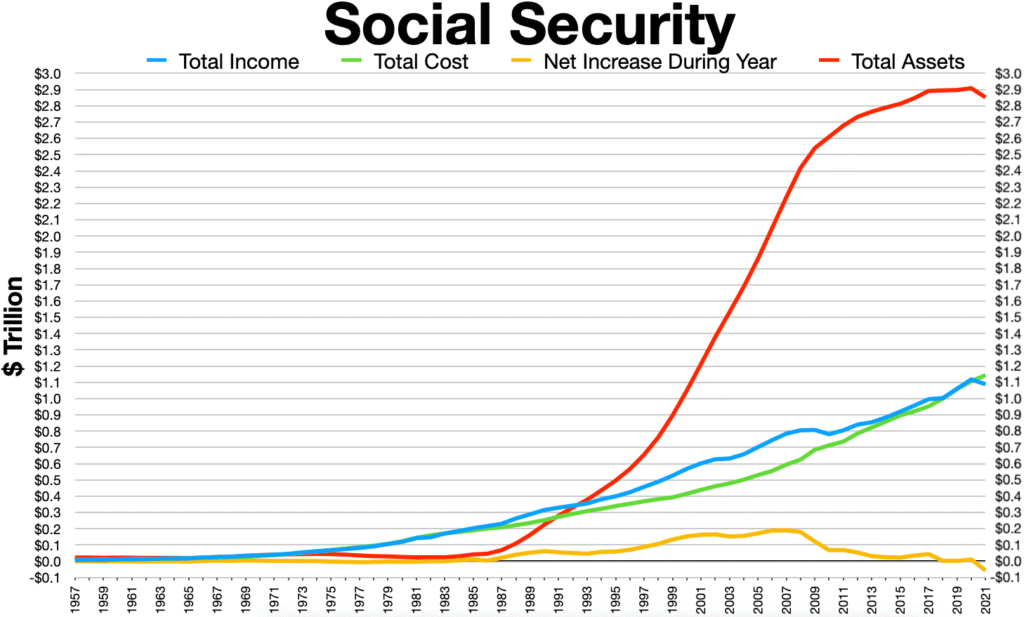

Trust-Fund & Financial Status

According to the Social Security Administration’s 2024 Trustees Report, the combined OASDI trust funds (Old-Age & Survivors Insurance plus Disability Insurance) are projecting a decline in reserves. The reserves are projected to shrink from $2,788 billion at the start of 2024 to about $551 billion by the end of 2033 under the “intermediate” assumption scenario.

What this means: While benefits continue now, future revisions such as tax increases, benefit formula adjustments or eligibility changes may be necessary to sustain the program.

Payroll Tax & Wage Base Changes

The OASDI program is funded largely through payroll taxes under the Federal Insurance Contributions Act (FICA). Employees and employers each pay 6.2% toward OASDI (12.4% total for self-employed).

For 2025, the taxable maximum (the wage base subject to OASDI tax) is $176,100.

Being aware of this wage base affects high-earning workers and self-employed persons planning their tax and retirement strategies.

Coverage & Program Basics

Nearly 96% of jobs in the United States are covered by OASDI. To qualify for retirement benefits, workers generally must accumulate at least 40 credits (typically 10 years of covered work) and are subject to rules about when to claim.

The program offers three major benefit categories: retirement, survivors (for family members of a deceased worker) and disability insurance.

Benefit Adjustments (COLA & Earnings Limits)

The SSA issues annual cost-of-living adjustments (COLA) that impact benefit levels. Keeping track of these and other updates (such as earnings limits for beneficiaries working while receiving benefits) is key for retirees.

For example, the wage base and earning limits increase periodically, and those changes influence both tax contributions and benefits.

Why These Updates Matter to You

For current and future retirees: The health of the OASDI program and the tax/wage-base changes affect how much you contribute now and what benefit you may receive later.

For disabled workers and survivors: Changes in the trust-fund status and eligibility rules could mean shifts in how benefits are calculated or structured.

For higher-income and self-employed individuals: The wage base and tax contribution rules directly affect your planning.

For advisors and legal professionals: Understanding recent updates is necessary to provide accurate counsel on retirement strategy, tax planning, or disability appeals.

Expert Legal Counsel & Firms for OASDI-Related Issues

If you are navigating complex questions about retirement, disability or survivor benefits under OASDI, or if you are facing benefit reductions, appeals or planning issues, these law firms in the U.S. specialize in relevant benefits and Social Security matters:

- Law Offices of Cory A. DeLellis – A California-based practice offering guidance on Social Security retirement and disability benefits. Website: corydelellislaw.com

- Ryan Bisher Ryan & Simons – Michigan law firm handling Social Security disability (SSDI) claims, retirement strategies and benefit appeals. Website: rbrlawfirm.com

- Seyfarth Shaw LLP – National law firm that represents employees and employers regarding Social Security, plan benefits, retirement and disability issues. Website: seyfarth.com

Before choosing counsel, ask about their track record with OASDI-related cases, whether they handle appeals, their fee structure, and how they stay current on regulatory/legislative changes.

Practical Steps to Take Now

- Review your Social Security statement – Log into your “my Social Security” account, check your earnings history, estimate your benefit, verify that your work credits are correct.

- Understand the tax & contribution implications – If you’re self-employed or a high earner, monitor how the wage base and tax contributions impact your long-term benefit.

- Update your retirement strategy – Given the trust-fund projection risks, avoid relying solely on OASDI; consider savings, private pensions, 401(k)/IRA, other sources.

- Monitor upcoming COLA and earnings-limit changes – Benefit amounts and eligibility rules may adjust yearly; staying ahead helps planning.

- If you’re disabled or applying for survivors benefits – Gather documentation early, consult a qualified attorney if your situation is complex, and review your eligibility and strategy now.

📚 You May Also Like

💡US Social Security Survivors Benefits News 2025: What Families Should Know About the Latest SSA Changes

Learn which U.S.-based attorneys provide the strongest legal representation and highest claim success rates this year.

🚗 Retirement Disability Benefits News USA: Latest Updates, Legal Insights, and What You Should Know

Explore top-rated U.S. attorneys helping victims maximize compensation for vehicle damage and medical expenses.

⚖️ Retirement, Survivors & Disability Insurance News: Why It Matters Now

Discover the pros and cons of managing your car insurance claim independently versus hiring a legal expert.

🔥 Social Security Retirement News USA: What You Need to Know

See how USA ranks and what factors drive up insurance rates across the country.